If you are thinking of buying a second hand house in Spain, this interests you 04/10/2021

There will be a tax change when buying a home in 2022

Congress accepted a bill that will modify the calculation of the Tax on Patrimonial Transmissions (ITP), the tax paid by those who buy a used home. From now on, the buyer will not pay taxes for what his second-hand house has cost him, if not for its market value (the reference value estimated by the General Directorate of the Land Registry). The Ministry of Finance ensures that this new law will enter into force in January 2022, which will affect all sales that are signed from this date, since it is not retroactive.

What does this modification suppose?

This tax will be calculated from real estate transaction prices provided by Notaries and Registrars. Therefore, it is not necessary to visit the property, nor will you have to know the state of conservation, materials used, if it is renovated ... This will affect the ITP (Tax on Patrimonial Transmissions) and the Tax on Inheritance and Donations (ISyD).

It will no longer be necessary to make a visit or an on-site check of the property sold, inherited or donated to know if the taxpayer has paid the correct value, the taxable base will be the reference value approved by the Cadastre.

If the taxpayer does not agree with the reference value, they will have to prove their mistake with evidence, the burden of proof falling on the taxpayer and they will have to demonstrate that the Land Registry reference value does not correspond to the market value.

How does it affect the buyer of a used home?

Currently, many times a value check is made, which is when the regional Treasury checks the value of the property purchased because it estimates that the buyer has paid less taxes than he should, where the new reference value based on the cadastre comes into play.

Due to the fact that the houses are valued above the notarized price, the autonomous estate ends up demanding from the buyer of a cheap house or the heir of a house a payment higher than that initially paid by the Property Transfer Tax (ITP) or the Inheritance Tax and Donations (ISD).

difference between market price and management value

Normally when this happens the regional Treasury opens a claim when it believes that the value of a sale or inheritance is higher than the price that was registered, according to the regional administrations or the reference value (when it comes into force in 2022). This modification of the extra property tax as a "complementary settlement of securities" that is accompanied by interest for late payment.

This tells us that there is a big difference between the market price and the value established by the administration.

And how are the CCAA going to determine the value of a house?

As of January 2022, it will be done with the new reference value approved by the General Directorate of the Land Registry. Therefore, the administration will not be obliged to send an expert to make a visit to the house sold, inherited or donated, so the seller who makes reforms to his house to revalue it before selling it will be punished considering that it is worth the same as a house in the same area without reforms.

Although this reference value has not yet been approved, it is envisaged that “When there is no reference value or it cannot be certified by the General Directorate of Cadastre, the taxable base, without prejudice to the administrative verification, will be the highest of the following magnitudes: the value declared by the interested parties or the market value ”.

Therefore, when the Land Registry reference value comes into force, taxpayers must declare in accordance with said value, because it is required by law.

How to act until the new Land Registry reference value comes into force?

This new rule provides that the taxable base of the properties will be this reference value based on the Cadastre, but until the new value comes into force the legal forecast remains incomplete.

For this reason, in 2021, the assessments will have to be made as before. Using any of the means provided in article 57.1 of the General Tax Law, claiming that the methods used are not adequate to obtain the market value of the property. And criticizing, depending on the case, the lack of a visit by the expert to the property, or the use of a means such as mortgage appraisal, reviled by several Superior Courts of Justice.

Therefore, this delay in the Land Registry in approving its reference value will give us a slight truce, before the new value checks take effect, once the reference value is applicable.

Be very careful with paying taxes according to the value of reference in case of deed for a higher amount!

With this new tax anti-fraud law, the taxpayer has the obligation to pay taxes for the taxed value if it is higher than the official value of the Autonomous Community. The new wording of article 10 of the Property Transfer Tax Law states that “if the value of the property declared by the interested parties, the agreed price or consideration, or both are higher than its reference value, the taxable base will be the greater of these magnitudes ”.

For example: If you buy a property for € 400,000 but the official valuation of the corresponding Autonomous Community is only € 290,000. Many taxpayers considered that, in this case, they are claiming the possibility of paying taxes for the official value of the Community, without exposing themselves to receiving a value check. And that article 46.3 of the Transmission Tax Law was not applicable in these cases.

How to challenge the new Land Registry reference value

There are two options to contest this reference value for which it is considered not to reflect the purchase value:

· Self-liquidate for the official value and immediately afterwards request the rectification of the self-assessment,

also challenging the reference value.

· Self-liquidate for the value that the taxpayer considers that the home has (usually the deed) and later appeal the verification of values that may come from the regional administration. Both settlement and the reference value will be used. In this case, the Tax Administration will resolve a previous mandatory and binding report from the General Directorate of the Land Registry, which ratifies or corrects the aforementioned value, in view of the documentation provided.

That is, it will be the Treasury who will request a report from the Land Registry to ratify or correct the reference value of the home purchased or inherited.

Taxes linked to the sale

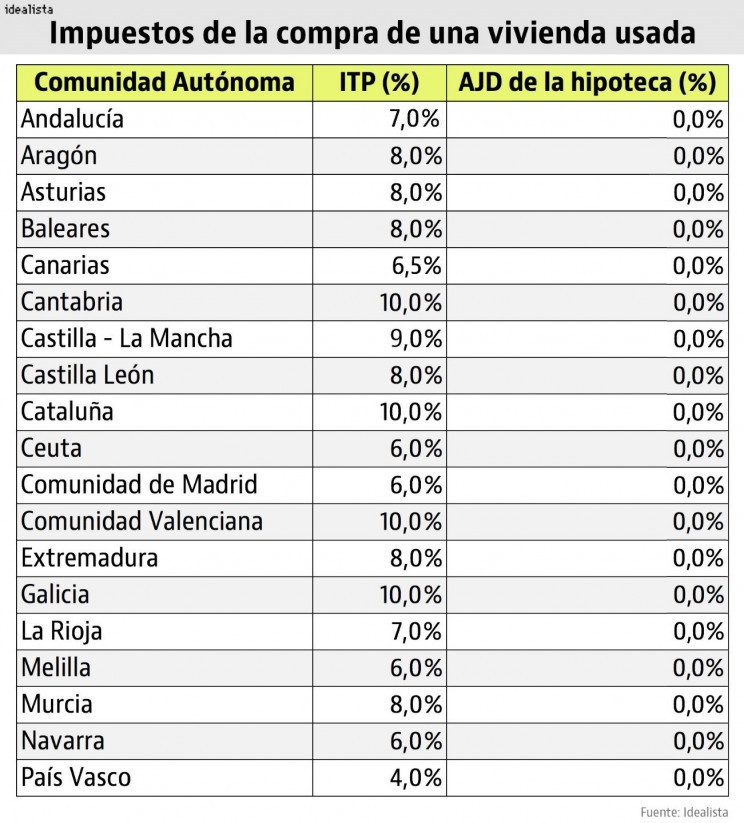

For second-hand homes, the most important tax is the Tax on Patrimonial Transmissions (ITP). In this case, it depends on the percentage that is applied on the notarized price and on the autonomous community in which the house is located, although as a general rule between 6% and 10% is applied. However, for VPO, large families and young people there are usually reduced rates. For example, in Madrid large families who buy a free home will pay a 4% ITP on the notarized price as long as the home purchased is the usual one. These types currently apply:

The agency, an optional expense

The agencies are usually the entities that the client can hire to process the tax settlement and manage other paperwork related to the purchase of the property. They are usually contracted when a mortgage is opened to acquire the property, its cost is usually around € 300, depending on the autonomous community and the services provided. However, if you need help to buy your property and need advice on the market, real estate laws or any other management on the property you want to acquire, you can receive free advice or help in legal procedures we can offer you exactly what you need, since we have more of 26 years building homes thanks to our team that has the experience and updating of the real estate market.